The Hidden Risks of Private Credit: Why Low Volatility Can Be Misleading

Recent market conditions highlight the risks of investing in private credit.

Recent headlines have put a spotlight on the private credit sector, to include articles detailing Blue Owl Capital’s recent sale of roughly $1.4 billion of loans from one of its funds.1 In a period defined by higher interest rates, tighter liquidity, and rising default expectations, sales like this carry greater significance. Economic conditions such as elevated borrowing costs and increased regulatory scrutiny give added weight to concerns around this sale. Taken together, these signals suggest that we are entering a more volatile phase for private credit.

What Private Credit Really Is and Why It Matters

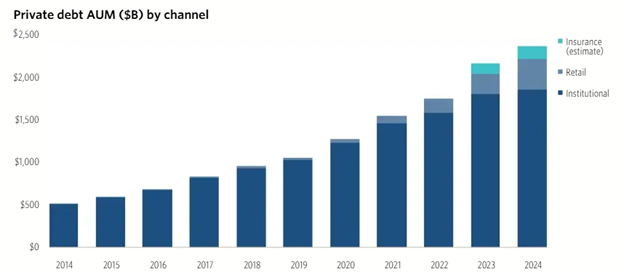

Private credit refers to loans made directly to companies outside of traditional banks or public bond markets.2 Unlike publicly traded bonds, these loans are illiquid, and therefore reported valuations tend to move gradually, giving the appearance of lower volatility compared with public bonds.3 Over the last 20 years, private credit has dramatically grown to be a major component of the lending market. Therefore, unlike the past, a credit problem in private credit could have broad economic implications.

Visual 1: Growth in Dollars of Private Credit funds since 2000

Source: Pitchbook – Geography Global – As of December 31, 2024

Note: Retail and Insurance figures are as of June 30, 2025

Illiquidity Can Mask Risk

Academically, risk is often defined as volatility. Under that definition, private credit appears “low risk.”4 However, from an investor’s standpoint, risk may be more accurately measured as the probability of permanent capital loss or an undesirable outcome. When measured this way, illiquid private credit can carry substantial risk.

Many private credit loans are extended to companies with high leverage or depend on refinancing markets staying open. If liquidity tightens or refinancing becomes more expensive, default probabilities rise. Compared with high-yield or investment-grade corporate bonds, private credit may have lower observed volatility but potentially higher severity of loss in stressed scenarios. Public bonds react immediately to changing credit conditions; private loans may not reflect economic stress until later, creating the illusion of stability.5

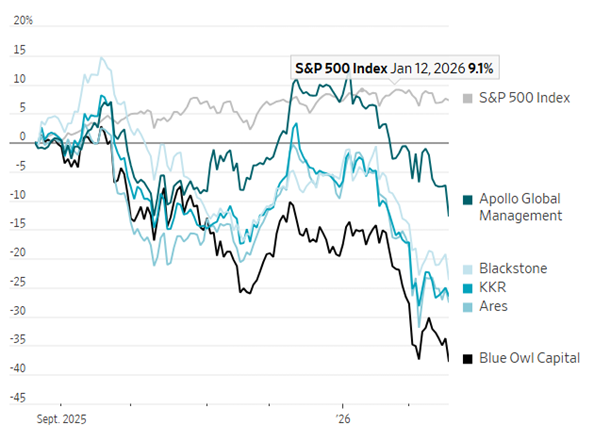

Visual 2: Private Credit fund managers stock performance vs. the S&P 500 Index from 2025 to 2026

Source: FactSet

Why Are People Paying Attention Now?

"Only when the tide goes out do you discover who's been swimming naked" - Warren Buffett

After Dodd-Frank was enacted, banks were limited when it came to lending money. Alternative lenders filled that space since they faced fewer regulatory capital constraints.7 As these alternative investors grew, they needed to generate more money to keep making loans. They began marketing to retail investors by creating funds with limited liquidity features. This attempted to attract retail investors by allowing a portion of the amount invested to be withdrawn periodically, which created an appearance of a liquid investment.8

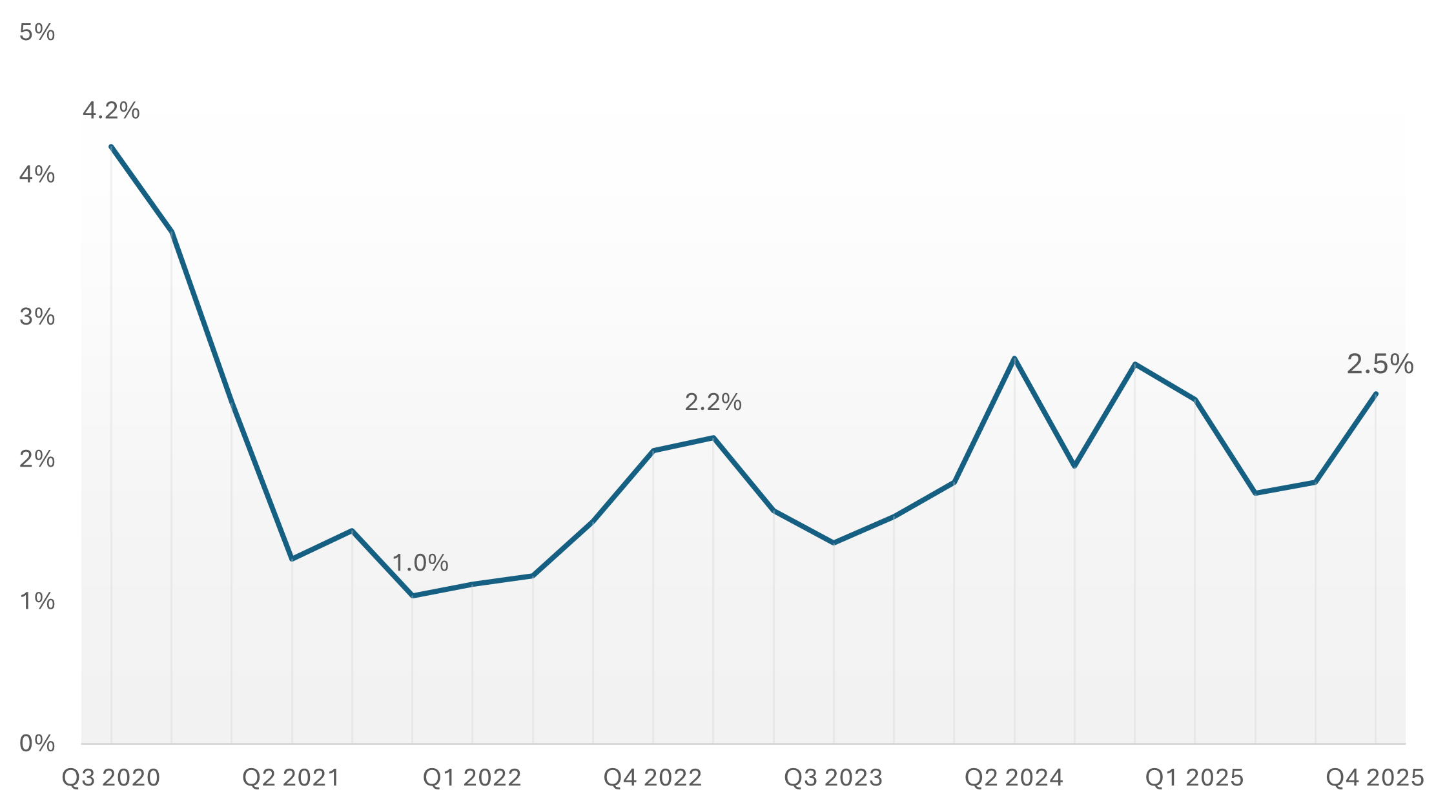

However, the environment is different now. Interest rates are higher, an increasing number of loans are coming due as time passes, and companies are now refinancing at higher rates.9 Of note, there was a sharp decline in private credit defaults between 2020 and 2021, but there has been a gradual rise in defaults since then. Major banks are warning of the sector’s increasing fragility.10

Visual 3: Percentage of Private Credit Defaults by Quarter (2020-2025)

Source: Proskauer press releases, directly cited

Note: Q1 2020 is approximate — the index launched mid-2020 and the inaugural release referenced Q1 retrospectively without a precise headline figure.

Even central banks are paying closer attention. The Bank of England has begun stress-testing private equity and private credit exposures, signaling that regulators consider the sector large enough and interconnected enough to warrant scrutiny.11

Public markets have reflected these concerns. Shares of major alternative asset managers, including Apollo Global Management, Blackstone Inc., Ares Management, and KKR & Co., have experienced notable volatility as investors digest the potential implications of rising defaults, liquidity mismatches, and regulatory attention.12

Conclusion

Recent developments in private credit have drawn attention to the risks in an asset class long perceived as stable. Private credit’s low volatility can create the appearance of stability, while masking underlying risks such as rising default probabilities, refinancing pressures in a higher-rate environment, and potential liquidity mismatches between investors and the underlying assets. As borrowing costs increase and regulators intensify oversight, concerns are growing that private credit’s muted price movements may underestimate the true risk of capital loss, especially in stressed economic conditions.

*Disclosure Statement: This material is provided by Chatham Capital Group for informational purposes only and is not intended as personalized investment, tax, or legal advice. Nothing contained herein constitutes a recommendation, solicitation, or offer to buy or sell any securities or to adopt any specific investment strategy. The views and strategies discussed may not be suitable for all investors. Individuals should consult with their financial, tax, and legal professionals before implementing any investment strategy.

Chatham Capital Group is an investment adviser registered with the U.S. Securities and Exchange Commission (“SEC”). Registration with the SEC does not imply a certain level of skill or training.

All investments involve risk, including the possible loss of principal. There can be no assurance that any investment strategy will be successful. Past performance is not indicative of future results. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.

Any references to market indices are for illustrative purposes only. Indices are unmanaged, cannot be invested in directly, and do not reflect the deduction of fees, expenses, or transaction costs. Index performance is not indicative of the performance of any client account.

Information presented is believed to be reliable; however, Chatham Capital Group makes no representation or warranty as to its accuracy, completeness, or timeliness. Any opinions expressed are subject to change without notice.

Any company names, securities, or third-party services referenced are for illustrative or educational purposes only and do not constitute an endorsement or recommendation. Unless otherwise stated, Chatham Capital Group is not affiliated with, and does not endorse, any third-party entities mentioned.

1. Wall Street Journal, “Private-Credit Warning Signs Flash After Blue Owl Unloads $1.4 Billion in Assets,” Accessed Feb. 20, 2026. https://www.wsj.com/finance/investing/private-credit-warning-signs-flash-after-blue-owl-unloads-1-4-billion-in-assets-02494fab?msockid=2cab0adaf968651c1d3e1c2ef8cf640a

2. Corporate Finance Institute, “What Is Private Credit?,” published Oct. 28, 2025, accessed Feb. 26, 2026. https://corporatefinanceinstitute.com/resources/capital_markets/what-is-private-credit/

3. AIMA Journal, “Unmasking Private Credit Risk: Beyond the Leveraged Loan Analogy,” by Lue Xiong, published Nov. 24, 2025, accessed Feb. 26, 2026. https://www.aima.org/article/unmasking-private-credit-risk-beyond-the-leveraged-loan-analogy.html

4. Encyclopedia Britannica, “Modern Portfolio Theory Explained,” Accessed Feb. 26, 2026. https://www.britannica.com/money/modern-portfolio-theory-explained

5. AIMA Journal, “Unmasking Private Credit Risk: Beyond the Leveraged Loan Analogy,” by Lue Xiong, published Nov. 24, 2025, accessed Feb. 26, 2026. https://www.aima.org/article/unmasking-private-credit-risk-beyond-the-leveraged-loan-analogy.html

6. Berkshire Hathaway, “1992 Chairman’s Letter to Shareholders — It’s only when the tide goes out that you learn who’s been swimming naked,” Accessed Feb. 26, 2026. https://www.berkshirehathaway.com/letters/1992.html

7. RSF: The Russell Sage Foundation Journal of the Social Sciences, “The Impact of the Dodd-Frank Act on Financial Stability and Economic Growth,” Accessed Feb. 26, 2026. https://www.jstor.org/stable/10.7758/rsf.2017.3.1.02

8. InvestmentNews, “Record growth: Interval funds emerge as key players in alternative investments,” Accessed Feb. 26, 2026. https://www.investmentnews.com/ria-news/record-growth-interval-funds-emerge-as-key-players-in-alternative-investments/259311

9. Reuters, “U.S. private credit defaults to ease in 2026, but fragility to persist, says BofA,” Reuters, Dec. 9, 2025. Accessed Feb. 20, 2026. https://www.reuters.com/business/finance/us-private-credit-defaults-ease-2026-fragility-persist-says-bofa-2025-12-09/

10. Reuters, “Blue Owl drops again as investors digest debt fund changes,” Reuters, Feb. 20, 2026. Accessed Feb. 20, 2026. https://www.reuters.com/business/finance/blue-owl-drops-again-investors-digest-debt-fund-changes-2026-02-20/

11. Reuters, “Bank of England launches stress test of private equity and private credit industries,” Reuters, Dec. 4, 2025. Accessed Feb. 20, 2026. https://www.reuters.com/sustainability/boards-policy-regulation/bank-england-launches-stress-test-private-equity-private-credit-industries-2025-12-04/

12. Financial Times, “Private credit stocks slide after Blue Owl halts redemptions at fund,” Financial Times, Feb. 19, 2026. Accessed Feb. 23, 2026. https://www.ft.com/content/cdca18df-473c-4c66-a6db-d9be32bf9d88