Roth IRA Conversions: A Practical Guide for Investors

Planning considerations for investors with substantial pre-tax retirement assets.

IMPORTANT DISCLOSURE: This article is provided for general informational and educational purposes only. It does not constitute investment advice, a solicitation, or a recommendation to buy or sell any security or investment product. Tax laws are subject to change; information presented reflects current law as of the date of publication and should not be relied upon as legal or tax advice. Past performance is not indicative of future results. All investments involve risk, including the possible loss of principal. Readers are strongly encouraged to consult a qualified financial advisor, registered investment adviser, and tax professional before making any decisions regarding their retirement accounts. Nothing in this article creates a fiduciary or advisory relationship of any kind.

Roth IRA conversions come up frequently in client conversations, and the potential benefits are real in the right circumstances. For most investors, the decision to convert is more complex than it first appears, and in many cases the right answer is to proceed carefully, convert only a limited amount, or not convert at all. It is important to have a framework for understanding what the decision actually involves and why it deserves careful, individualized analysis. The following is a practical guide to the process, the account-specific nuances for SEP and SIMPLE IRA holders, and the planning considerations that matter most before making this decision.

What a Roth Conversion Actually Does

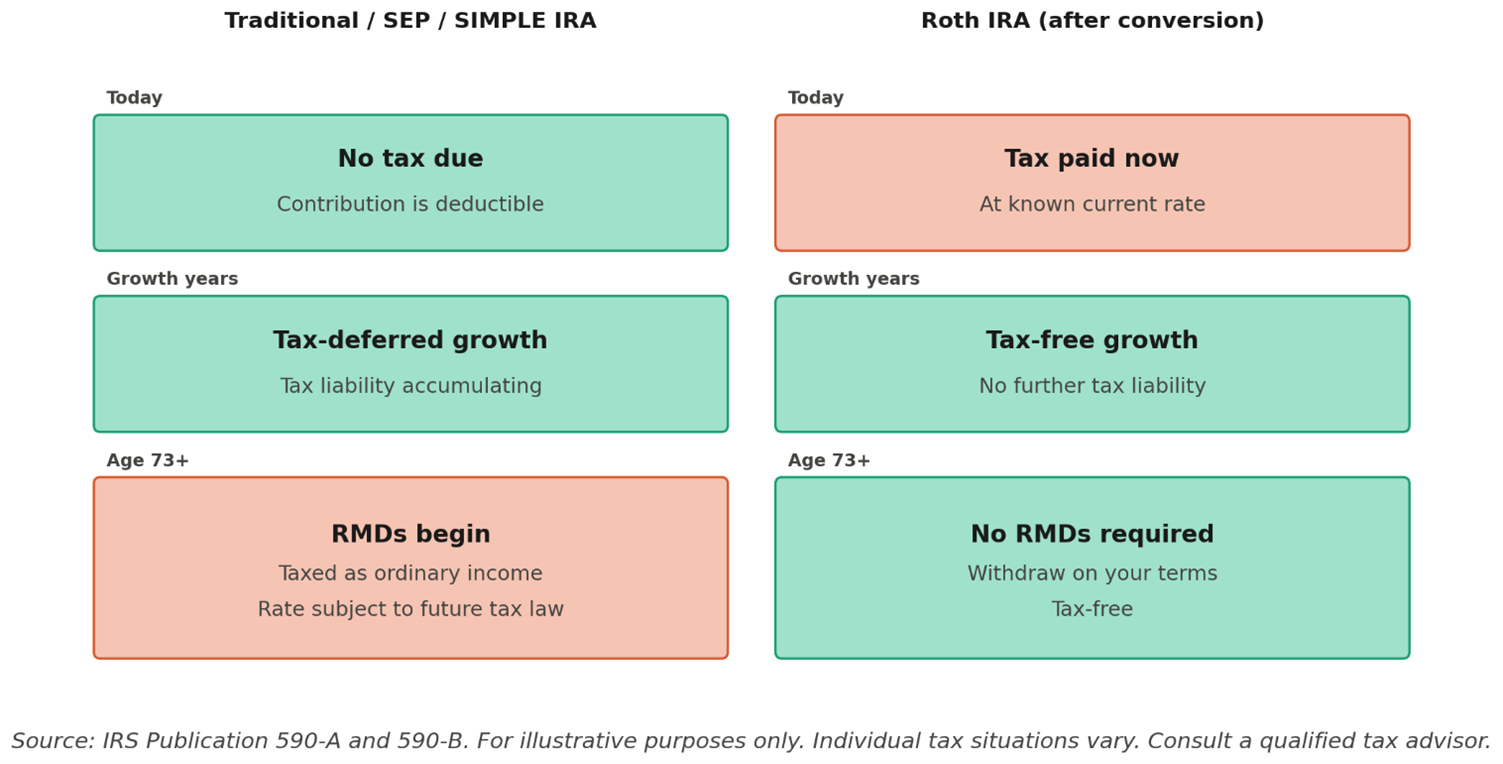

A Roth IRA conversion moves pre-tax retirement assets, including funds in a traditional IRA or SEP IRA, into a Roth IRA. The amount you convert is added to your ordinary taxable income in the year the conversion takes place. You pay income tax on it now, at your current rate. In exchange, the funds in the Roth IRA grow tax-free, and qualified withdrawals in retirement are not subject to federal income tax. 1 The Internal Revenue Code imposes no income limit on who can execute a conversion. While direct contributions to a Roth IRA are restricted for higher earners, conversions carry no such restriction. 2 Anyone with a pre-tax IRA, regardless of income, can convert.

Investors typically convert for one of two reasons:

Avoiding forced distributions. Non-Roth IRAs require distributions beginning at age 73, taxed as ordinary income regardless of whether you need the funds. For investors with substantial balances who plan to live off other income sources in retirement, those mandatory withdrawals can push taxable income into higher brackets at a time when there is little flexibility to manage the timing or amount. Roth IRAs are not subject to RMDs during the account owner's lifetime. 6,7 Converting a portion of pre-tax assets before age 73 reduces the balance subject to forced distributions and gives you more control over how you draw down your savings.

Locking in a known tax rate. A conversion establishes your tax liability in the current year, at today's known rates, rather than leaving it subject to whatever the rate environment looks like in the future. For investors who expect their tax burden to be higher in retirement than it is today, paying the tax now can be the more efficient path.

Visual 1: Tax treatment at each stage: traditional IRA vs. Roth IRA after conversion

Roth Conversions for SEP IRA and SIMPLE IRA Holders

SEP IRAs and SIMPLE IRAs are pre-tax retirement accounts commonly used by self-employed individuals, small business owners, and their employees. Both are eligible for Roth conversion, and the full converted amount is subject to ordinary income tax, since every dollar that went in was tax deductible.4

It is worth understanding how this differs from a non-deductible IRA conversion. Some investors make traditional IRA contributions for which they take no tax deduction, putting funds in on an after-tax basis. When those contributions are later converted to a Roth, the previously taxed portion is generally not subject to income tax again at conversion, since the investor has already paid tax on those contributions. By contrast, SEP and SIMPLE IRA contributions are always fully deductible, which means there is no after-tax basis to offset and the entire converted amount is taxable. For investors with substantial balances in these accounts, the tax liability of a full conversion can be substantial. Converting in pieces over multiple years, particularly during lower-income years, is generally the more practical approach.5

There is one important distinction between SEP and SIMPLE IRAs. A SEP IRA can be converted to a Roth at any time. A SIMPLE IRA, however, cannot be converted until two years have passed from the date you first participated in the plan. Attempting to convert before that two-year window closes triggers a 25% early distribution penalty in addition to the ordinary income tax owed on the converted amount.4

One additional opportunity worth noting: converting a SEP or SIMPLE IRA does not prevent future contributions to a new plan of the same type. Business owners who continue generating income can keep contributing to a SEP or SIMPLE IRA and convert those new contributions over time, creating a repeating conversion window during lower-income years.

When a Conversion May Not Be the Right Move

Roth conversions receive considerable attention, but they are not the right strategy for every investor. Understanding when a conversion does not make sense is just as important as understanding when it does.

A conversion is unlikely to make sense if any of the following apply:

You are already in the top federal tax bracket with no near-term window of lower income. The core logic of a Roth conversion is paying tax at a known rate today to avoid paying more later. If your current rate is already at or near the maximum, that logic does not hold.

You cannot fund the tax bill from outside the IRA. If you do not have non-retirement assets available to cover the tax bill, the conversion becomes significantly less advantageous. Using converted funds to pay the tax reduces your Roth balance from the start and can diminish the long-term benefit.

Your time horizon is shorter. The tax-free growth inside the Roth needs several years to offset the upfront tax cost. For investors later in retirement with a shorter time horizon, the less likely the conversion makes financial sense.

Your estate planning objectives favor pre-tax assets. Leaving traditional IRA assets to a surviving spouse with lower income, or to a charitable beneficiary, can in certain situations be more tax-efficient than converting. The right answer depends on the full estate picture.

None of this means a conversion is categorically off the table for these investors. It means the analysis is more difficult, the margin for error is smaller, and the case for proceeding needs to be stronger. For many investors, a Roth conversion is worth understanding but not necessarily worth doing, and distinguishing between the two requires a careful look at the full financial picture.

The Case for Partial Conversions

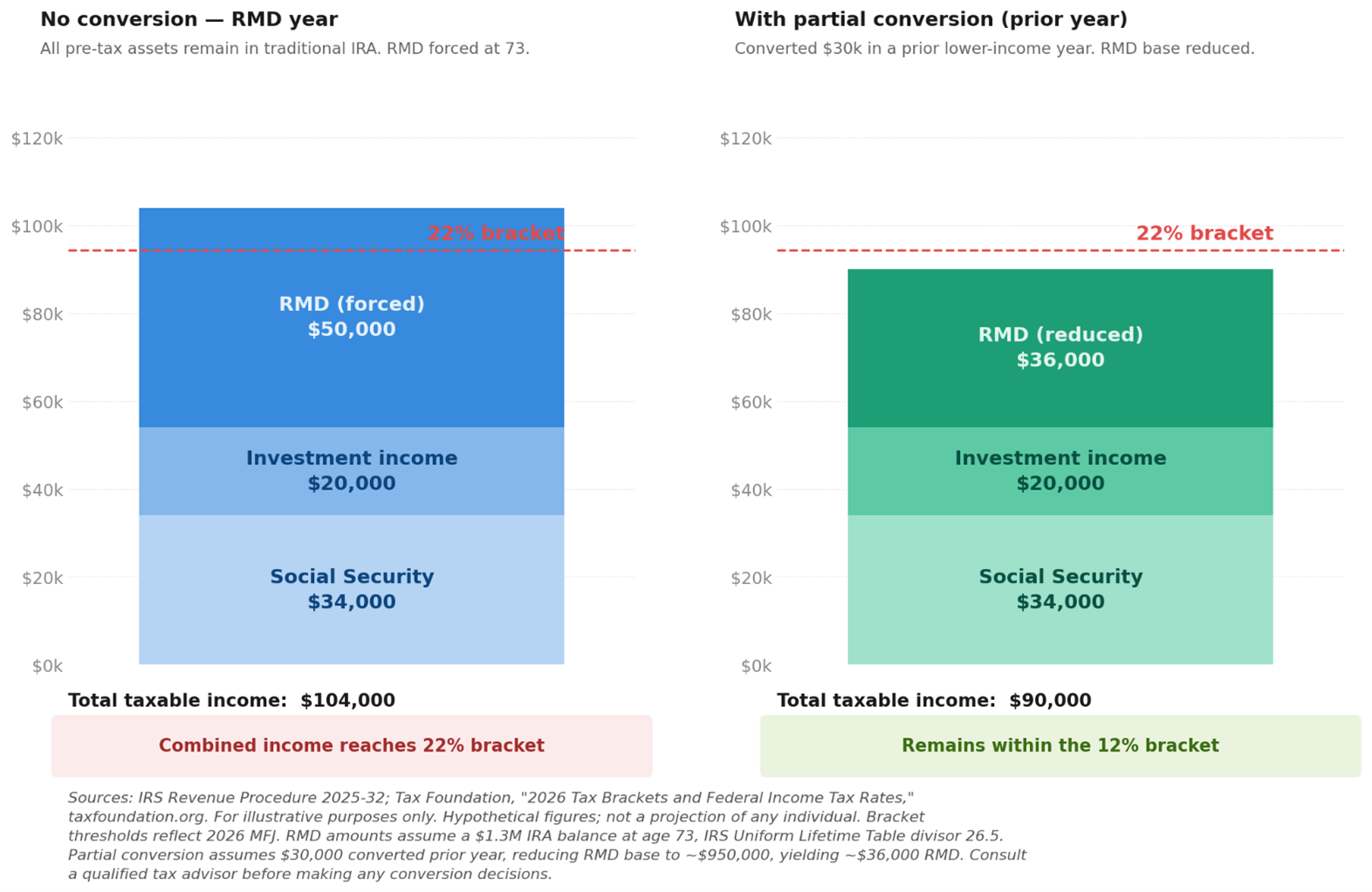

For investors with large balances, converting everything in a single year is rarely the right approach. A full conversion of a large SEP IRA or traditional IRA could push income into the highest federal tax bracket, generate IRMAA (Income-Related Monthly Adjustment Amounts), and create a material state tax bill, all in the same year.8,9

A more common approach is bracket filling: converting a targeted amount each year that brings total income to the top of your current tax bracket without crossing into the next. The goal is not to eliminate the tax on your retirement savings. It is to pay it at a known rate, in a controlled way, over time, rather than having it imposed by RMDs at whatever rate applies in the future.6

For investors with a meaningful gap between now and age 73, this approach can be executed over a number of years, spreading the tax cost while progressively reducing the RMD base. For investors closer to that threshold, the window is shorter and the annual conversion amounts may need to be larger to have a noticeable impact.

Visual 2: Income stacking: with partial conversion vs. without

Key Considerations Before Converting

Conversions are permanent. Since the Tax Cuts and Jobs Act of 2017, Roth conversions cannot be undone. Prior to 2018, a conversion could be reversed through a process called recharacterization if circumstances changed. That option no longer exists under federal law. This makes careful planning before executing a conversion especially important, and investors should confirm any state-specific implications with a qualified tax advisor.3

A conversion affects more than just your tax bracket. A conversion adds to your ordinary taxable income for the year, and the consequences extend beyond the rate applied to the converted amount. Depending on your total income, conversion income can push you into a higher bracket and cause other investment income such as dividends and capital gains to become subject to the 3.8% Net Investment Income Tax surtax. This is why modeling the full picture, not just the converted amount in isolation, matters before executing a conversion in any given year.8,9

How conversion income affects your Medicare premiums. For investors over 63, conversion income can trigger or increase IRMAA. These are surcharges on Medicare Part B and Part D premiums, calculated based on income from two years prior. A large conversion today can affect premiums two years from now.8 For investors already in the upper tiers of IRMAA, additional conversion income may carry a real cost that belongs in the analysis.

Whether you can pay the tax from outside the IRA. If you use retirement funds to cover the taxes owed on a conversion, you reduce the amount actually working for you inside the Roth. The benefit is greatest when taxes are paid from non-retirement assets.1 For investors with significant taxable investment accounts or cash reserves, this is often feasible. For those who would have to fund the tax bill from the converted funds themselves, the benefit diminishes meaningfully.

The pre-RMD window. The years between retirement and age 73 can represent a planning window for some investors. If you have stepped back from full-time work but have not yet started Social Security, your income may be lower than it was during peak earning years. Converting during this period, what some planners call the 'income valley,' may allow you to convert funds at a reduced tax cost before the RMD clock begins.6 This window varies significantly by individual, however. Investors with ongoing business income, rental income, pensions, board compensation, or other passive income sources may find their income remains elevated throughout retirement, in which case the income valley is narrower or absent entirely, and the conversion calculus changes accordingly.

State income taxes. Not all states treat retirement income the same way. Some states exempt IRA distributions and conversions from state income tax entirely. Others tax them at the full state rate. If you live in a state with meaningful income taxes, that adds to the cost of conversion. If you are planning to relocate to a lower-tax state before or during retirement, that timing may affect when a conversion makes most sense.

Georgia. Georgia generally exempts retirement income from state income tax for residents age 62 and older, up to limits that are adjusted periodically. Roth conversion income is treated as ordinary income in the year of conversion, and whether Georgia's retirement income exemptions apply to converted amounts depends on the taxpayer's age, total income, and other factors at the time of conversion. Georgia residents should confirm the current treatment of Roth conversion income with a qualified state tax advisor before executing a conversion, as state tax law is subject to change. See O.C.G.A. § 48-7-27.9

South Carolina. South Carolina provides a retirement income deduction for residents age 65 and older; residents below age 65 may qualify for partial deductions depending on the nature and source of the retirement income. Roth conversion income is treated as ordinary income in the year of conversion under South Carolina law, and whether the state's retirement income deductions apply to converted amounts depends on the taxpayer's age, total income, and other factors at the time of conversion. South Carolina residents should confirm the current treatment of Roth conversion income with a qualified state tax advisor before executing a conversion, as state tax law is subject to change. See S.C. Code Ann. § 12-6-1170.9

Estate planning. Roth IRAs can be a tax-efficient vehicle for transferring wealth. When a non-spouse inherits a Roth IRA, distributions are generally income-tax-free, subject to the 10-year rule established under the SECURE Act.10 The specific requirements within that 10-year window, including whether annual distributions may be required for certain beneficiary categories, remain subject to ongoing IRS regulatory guidance and should be reviewed with a qualified tax advisor before relying on them for estate planning purposes. For investors whose retirement assets are likely to be passed to heirs rather than spent, the potential estate planning benefit of Roth assets is real, but the details of how that benefit applies to a specific situation require individualized analysis.

Legislative considerations. The individual income tax rates established by the Tax Cuts and Jobs Act of 2017 were made permanent by the One Big Beautiful Bill Act, signed into law on July 4, 2025.12 The current rate structure, including lower individual rates, the enhanced standard deduction, and the 20% pass-through deduction for qualified business income, is not set to expire under current law, though tax law remains subject to future Congressional action. The law also introduced a temporary additional deduction of $6,000 for individuals age 65 and older through 2028, which phases out above certain income thresholds and may provide some additional room in a conversion year for qualifying investors.12 For investors evaluating a Roth conversion, the current legislative environment provides more certainty than it did prior to 2025, but working with a qualified tax professional who stays current on the law remains an essential part of the analysis.

The five-year rule on earnings. The first five-year rule governs when earnings inside a Roth IRA can be withdrawn tax-free. To qualify, the account holder must be at least 59½ and the Roth IRA must have been open for at least five years from the date of the first contribution or conversion to any Roth IRA. This clock runs once per taxpayer, not per account.11

The five-year rule on converted amounts. The second rule applies specifically to converted amounts. Each conversion starts its own separate five-year clock. Withdrawals of converted principal before that five-year period, and before age 59½, may be subject to the 10% early withdrawal penalty, even though the converted funds themselves are not subject to income tax again.11 For investors executing multi-year conversion strategies, each tranche of converted funds carries a separate clock, and tracking them individually matters if there is any possibility of needing access to those funds before the relevant period has elapsed.

Conclusion

A Roth conversion analysis runs through a deeply personal set of variables: your current income, your expected retirement income, your timeline, your estate goals, your state of residence, your Medicare situation, and your heirs' likely tax circumstances. For some investors with substantial pre-tax assets, it may represent a genuine planning opportunity. For many others, the timing, tax burden, or estate situation argues against converting, or for converting only in limited amounts over time.

Whether a conversion makes sense is a question that belongs in a broader conversation about your full financial picture, one that accounts for your income, your timeline, your estate, and your goals. Every investor's situation is different, and the only analysis that matters is the one built around yours.

ENDNOTES

1. Internal Revenue Service. "Roth Conversions." IRS Publication 590-A, Contributions to Individual Retirement Arrangements (IRAs). Available at: irs.gov.

2. Internal Revenue Service. "Amount of Roth IRA Contributions That You Can Make." IRS Publication 590-A. Income phase-out thresholds for direct Roth IRA contributions are adjusted annually by the IRS. Current figures should be confirmed at irs.gov. Note: Income limits apply to direct Roth IRA contributions only; no income limit applies to Roth conversions.

3. Tax Cuts and Jobs Act of 2017, Pub. L. No. 115-97, § 13611 (2017), eliminating IRA recharacterization for Roth conversions at the federal level effective January 1, 2018. State tax treatment of conversions may differ; investors should confirm state-specific implications with a qualified tax advisor.

4. Internal Revenue Service. "SEP Plan FAQs" and "SIMPLE IRA Plan FAQs." Available at: irs.gov. SEP IRA contributions are limited to the lesser of 25% of net self-employment compensation or an annually adjusted dollar ceiling; SIMPLE IRA contribution limits are also adjusted annually. Both account types accept only pre-tax contributions. SEP IRAs may be converted to a Roth IRA at any time. SIMPLE IRAs may not be converted until two years have elapsed from the date of first participation in the plan; distributions taken before the two-year period are subject to a 25% additional tax. See also 26 CFR § 1.408A-4. Current contribution limits for both account types should be confirmed at irs.gov.

5. Internal Revenue Service. Form 8606, Nondeductible IRAs. Used to track after-tax contributions to traditional IRAs and calculate the taxable portion of IRA distributions and Roth conversions under the pro-rata rule. Under the pro-rata rule, all traditional, SEP, and SIMPLE IRA balances are treated as a single pool when determining the taxable portion of any conversion. See also IRC Section 408. Available at: irs.gov.

6. SECURE 2.0 Act of 2022, Pub. L. No. 117-328. RMD age increased to 73 beginning in 2023 for individuals who turn 72 after December 31, 2022. See also Internal Revenue Service, IRS Publication 590-B, for RMD calculation methodology and applicable distribution periods.

7. Internal Revenue Service. "Roth IRAs." IRS Publication 590-B, Distributions from Individual Retirement Arrangements. Roth IRAs are not subject to RMD rules during the account owner's lifetime. Available at: irs.gov.

8. Centers for Medicare and Medicaid Services. "Income-Related Monthly Adjustment Amounts." CMS Publication, updated annually. IRMAA surcharges are determined based on modified adjusted gross income from two years prior to the premium year. Available at: cms.gov.

9. Internal Revenue Service. "Questions and Answers on the Net Investment Income Tax." Section 1411 of the Internal Revenue Code. NIIT thresholds are set by statute and subject to legislative change; current thresholds should be confirmed at irs.gov. For Georgia state income tax treatment of retirement income, see O.C.G.A. § 48-7-27. For South Carolina state income tax treatment of retirement income, see S.C. Code Ann. § 12-6-1170. State tax laws are subject to change; residents should confirm current treatment with a qualified state tax advisor.

10. SECURE Act of 2019, Pub. L. No. 116-94. Established the 10-year rule for non-spouse inherited IRAs. Non-spouse beneficiaries of inherited Roth IRAs are generally not subject to income tax on qualifying distributions but must distribute the full balance within 10 years of the original owner's death. Note: IRS proposed and final regulations under the SECURE Act continue to evolve; readers should consult a qualified tax advisor for current guidance.

11. Internal Revenue Service. IRS Publication 590-B, Distributions from Individual Retirement Arrangements. Two separate five-year clocks apply to Roth IRAs: one governing tax-free treatment of earnings (runs once per taxpayer from date of first Roth contribution or conversion), and one per conversion governing the 10% early withdrawal penalty on converted principal (runs separately for each conversion tranche). Available at: irs.gov.

12. One Big Beautiful Bill Act, signed into law July 4, 2025, Pub. L. No. 119-21. The Act made the individual income tax provisions of the Tax Cuts and Jobs Act of 2017 (Pub. L. No. 115-97) not subject to a scheduled expiration under current law, including lower individual tax rates, the enhanced standard deduction, and the 20% deduction for qualified pass-through business income under Section 199A. The Act also introduced a temporary additional deduction of $6,000 for individuals age 65 and older, effective 2025 through 2028, subject to income phase-outs. Tax law remains subject to future Congressional action; readers should confirm current law with a qualified tax advisor. For current IRS guidance see irs.gov.

DISCLOSURE STATEMENT

This article is provided by Chatham Capital Group for general informational and educational purposes only. It does not constitute investment advice, financial planning advice, legal advice, tax advice, or a solicitation or offer to buy or sell any security or investment product. This material has not been tailored to the investment objectives, financial situation, risk tolerance, or specific needs of any individual reader.

The information in this article reflects the views and research of Chatham Capital Group as of the date of publication and is subject to change without notice. No representation is made that the information is accurate, complete, or current. Tax laws and IRS figures referenced reflect current law and published guidance as of the date of publication and are subject to change; all figures should be independently verified before making any financial decisions.

Nothing in this article creates a fiduciary, advisory, or client relationship of any kind. Readers are strongly encouraged to consult with a qualified financial advisor, registered investment adviser, and tax professional before making any decisions regarding their retirement accounts. Chatham Capital Group's Form ADV Part 2A (Brochure) is available through the SEC's Investment Adviser Public Disclosure database at www.adviserinfo.sec.gov. Chatham Capital Group's Client Relationship Summary (Form CRS) is available at www.chathamcapitalgroup.com/s/Form-CRS.pdf.

Contribution limits for SEP IRAs, SIMPLE IRAs, and traditional IRAs are adjusted annually by the IRS. Current limits should be confirmed at irs.gov before making any contribution decisions. This material is not an advertisement for investment advisory services. Chatham Capital Group is a registered investment advisory firm headquartered in Savannah, Georgia.